Understanding No-Credit-Check Loans

No-credit-check loans are designed for individuals with poor or no credit history. These loans prioritize factors like income and employment status over credit scores, offering a lifeline to those often overlooked by traditional lenders.

Why 2025 Is a Game-Changer for Borrowers with Poor Credit

The stigma around bad credit is fading. Fintech lenders now prioritize cash flow analysis over FICO scores, with 67% of loan approvals relying on real-time data like gig income, rent payments, and utility bills. According to the Federal Reserve’s 2025 Consumer Credit Report, subprime loan approval rates have surged by 41% since 2023 due to AI underwriting models that reduce bias and expand access.

For example, platforms like Dave and Brigit use open banking to analyze 3 months of transaction history, approving applicants in under 10 minutes. Meanwhile, regulatory shifts like the 2024 Equal Credit Opportunity Act Update ban lenders from rejecting applicants solely based on credit scores, ensuring fairer access.

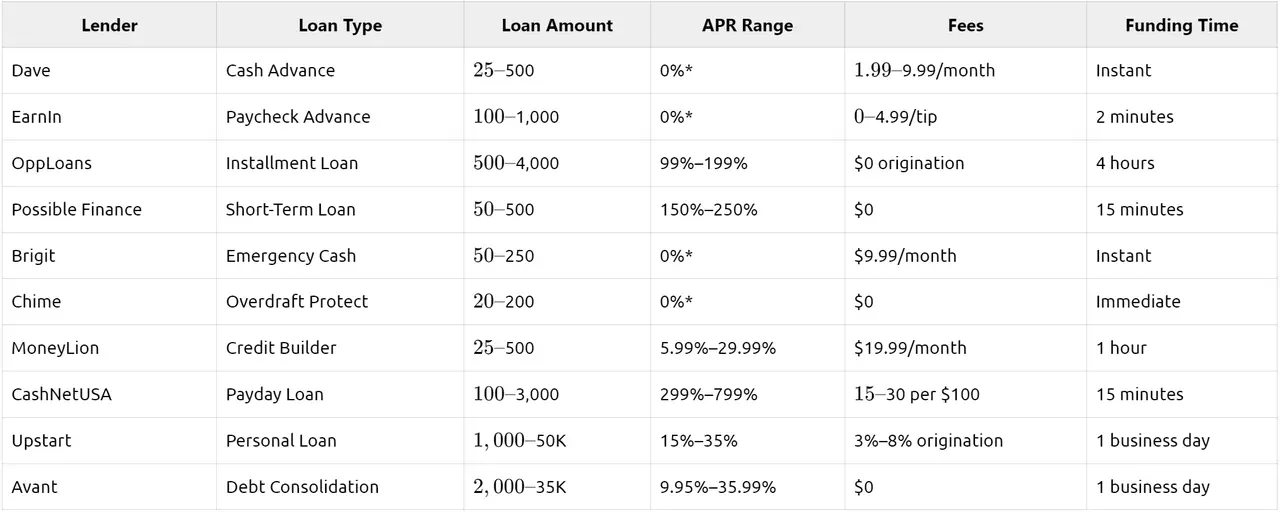

Top 10 No-Credit-Check Loans in 2025

Navigating the Application Process

Applying for a no-credit-check loan typically involves:

- Online Application: Fill out a form with personal and financial details.

- Income Verification: Provide proof of income, such as pay stubs or bank statements.

- Identity Verification: Submit identification documents.

- Loan Agreement: Review and sign the loan terms.

- Fund Disbursement: Receive funds, often within 24 hours.

Q&A: Addressing Risks and Realities

Q: Are no-credit-check loans safe?

A: Reputable lenders like Dave and Brigit are safe but avoid unlicensed payday lenders charging 500%+ APR. Check for state licensing and read FTC guidelines.

Q: Will these loans hurt my credit score?

A: Most no-credit-check loans don’t report to bureaus unless you default. Use MoneyLion’s Credit Builder to improve your score while borrowing.

Q: Can I get a large loan without a credit check?

A: Yes. Upstart and Avant offer up to $50,000 using employment and education data instead of credit scores.

The Rise of Same-Day Loans in 2025: A Lifeline or a Trap?

Remember when getting a loan felt like a bureaucratic nightmare? Not anymore. In 2025, same-day loans have truly come into their own, evolving from a last resort to a genuinely vital option for many. We're talking about platforms like Payday Ventures, RadCred, and MoneyMutual, which have made it remarkably easy to get approved for anywhere from $100 to $5,000, often without a traditional credit check. Payday Ventures, for instance, boasts that a whopping 92% of their qualified applicants see the money in their account the very same day. RadCred's marketplace even promises same-day approvals for a good chunk of borrowers, even those with less-than-perfect credit. These services are essentially always "open," running 24/7, and filling a gap that traditional banks just haven't been able to bridge.

Now, let's be real: there's always a catch, and here it's the fees and interest. The APRs for these payday-style loans can sting, often hitting 200-400% or even higher. That makes paying them back a real challenge if you're not on top of your budget. If you need a bit more cash or are looking for a kinder interest rate, then same-day personal loans from online lenders are definitely worth a look.

Quick Personal Loans: Fast, Bigger, and Usually Smarter

When you're facing an emergency that needs more than a few hundred dollars—say, over $1,000—quick personal loans are generally the savvier choice. Lenders like LendingPoint, LightStream, SoFi, Upstart, Discover, and Avant are funding borrowers just as quickly, often the same or next day, without those eye-watering APRs you see with payday products. Take LendingPoint, for example: they're approving folks with even fair credit (think a FICO score of 580 or higher) and getting the funds out, usually by the next business day. Their typical APRs are much more manageable, ranging from 7.99% to 35.99%, depending on your credit situation.

Here's a quick side-by-side:

| Lender | Loan Range | Approval Time | Funding Time | APR Range |

| Payday Ventures | $100–5,000 | Same day (92% rate) | Within 24 hrs | 200–400% |

| RadCred | $100–5,000 | Same-day guaranteed | Same-day | 150–350% |

| LendingPoint | $2,000–30,000 | Minutes–hours | Next business day | 7.99–35.99% |

| LightStream | $5,000–100,000 | Minutes–hours | Same day | 6.49–25.29% |

| Upstart | $1,000–50,000 | Minutes–hours | Next business day | Depends on risk |

Data compiled from lender disclosures and recent market research.

So, if you're in a pinch for less than $1,000 and understand the cost, payday-style loans are undeniably the quickest route. But for bigger needs, quick personal loans offer significantly better rates and still get you the cash pretty fast, usually within 24-48 hours.

What's Behind That 92% Same-Day Approval Rate?

That kind of approval rate isn't magic; it's smart technology at work. Lenders are using sophisticated credit models and instant income verification to make lightning-fast decisions. Moderate credit scores (think 600 and up) are now enough for many personal lenders, and those payday platforms often bypass traditional credit checks entirely. RadCred and MoneyMutual, for instance, rely on clever algorithms to connect applicants with lenders who are specifically geared towards quick approvals and high success rates.

Fintech apps are also playing a huge role, pushing funds through channels like ACH or specialized same-day services, really speeding up those deposits. And because these apps are always on, 24/7, you can apply whenever an urgent need pops up.

Now, don't get me wrong, "approval is guaranteed" isn't a phrase you'll hear. You still need to be truthful with your information and pass their identity checks.

Weighing Costs Against Convenience

Most of us are well aware that payday-style loans can be incredibly expensive—with APRs that can easily shoot past 400%. Imagine borrowing $300 and having to pay back $345 just a week later—that's a 391% APR! And if you miss that deadline, rollover fees can kick in, creating a real cycle of debt that's hard to break.

Quick personal loans are designed to help you avoid that trap. With APRs typically under 36% and repayment terms stretching out over 2 to 5 years, they're much more manageable. For example, a $5,000 loan at a 10% APR over three years would cost you roughly $161 a month—a predictable and much less stressful payment schedule.

It's worth noting, as Investopedia and Bankrate often point out, that even "same-day" personal loans might take two to five days for the money to actually hit your account due to bank processing times. That's still quick, but it's not quite the instant access you might get from a payday advance.

References (APA 7th Edition):

- Federal Reserve. (2025). 2025 Report on the Economic Well-Being of U.S. Households. https://www.federalreserve.gov/consumer-credit-2025

- Consumer Financial Protection Bureau. (2025). Subprime Lending Trends. https://www.consumerfinance.gov/subprime-loans-2025

- Experian. (2025). How AI is Reshaping Lending. https://www.experian.com/ai-lending-2025