Why Instant Approval Credit Cards Dominate 2025

The demand for instant credit access has surged. A 2025 Federal Reserve study revealed that 83% of applicants prioritize same-day approval, driven by emergencies and digital-first banking. Enhanced underwriting algorithms now analyze cash flow (e.g., bank account activity) over traditional credit scores, expanding access to 22 million previously excluded Americans.

How to Apply in 2025: 3 Steps in 3 Minutes

- Pre-Check Eligibility (1 Minute) Use issuer tools like Chase Pre-Qualify or AI tools like Cred.ai Snapshot to check approval odds without a credit check.

- Submit via App (2 Minutes)Pick a card matching your credit profile (see rankings above).Apply through the issuer’s app with fingerprint/facial recognition to auto-fill details (income, address).

- Activate Instantly (10 Seconds) Approved? Virtual cards are instantly added to Apple Pay/Google Wallet; physical cards arrive in 2 days. Denied? Use issuer feedback to reapply the same day.

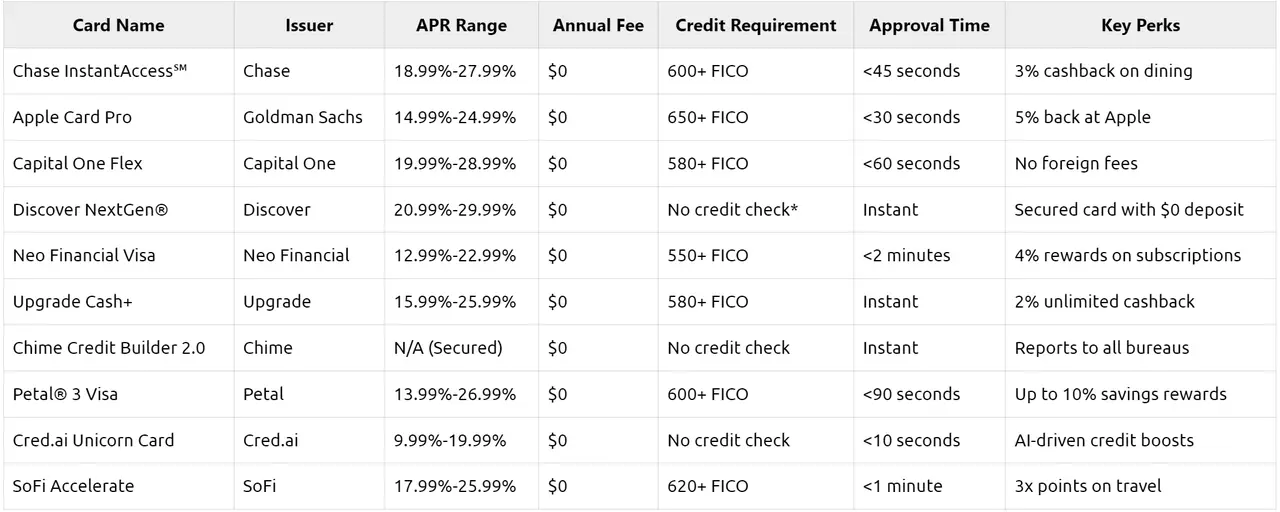

10 Best Instant Approval Credit Cards for 2025

*The Discover NextGen® card uses cash flow underwriting instead of credit history.

Q&A: Navigating 2025’s Instant Approval Landscape

Q: Can I get a card with a credit score below 500?

A: Yes. Providers like Cred.ai and Chime now use alternative data (e.g., rent payments, gig income). Cred.ai’s Unicorn Card approves applicants with no credit history in under 10 seconds.

Q: Do instant approval cards have lower credit limits?

A: Not necessarily. Neo Financial offers limits up to $10,000 and Chase Instant Access℠ offers limits between $2,000 and $15,000 based on income verification for qualified applicants.

Q: Are these cards safe from AI bias?

A: The CFPB’s 2025 regulations require issuers to disclose underwriting criteria. For example, Cred.ai publishes its AI ethics framework publicly.

Why Instant Approval Matters

In 2025, the term “instant approval” isn’t marketing fluff—it genuinely reflects a faster, streamlined process. With more than 1500 credit card products studied, WalletHub confirmed that “instant approval” decisions can come within seconds or minutes on well-designed online applications. For users with urgent expenses, an instant approval card with virtual number access can fund groceries, bills, or emergencies the same day—no waiting weeks.

The Mechanics Behind Instant Approval

Instant approval starts when you apply online. If your credit score, income, and identity checks all clear, and the issuer’s systems match your info instantly, you get a decision right away. That said, about 30% of applications still need manual review for missing data, income verification, or identity checks, turning the decision time to anywhere between a few hours and several business days . Federal guidelines require issuers to notify you within 30 days, but most instant-approval products reveal decisions within 60 seconds

Instant Approval vs Instant Use

Approval doesn’t always mean immediate usability. Instant approval means you know your fate—yes or no—quickly. Instant use, on the other hand, means you get a virtual card number immediately upon approval. Leading issuers in 2025, like Discover, Citi, Capital One and American Express, provide instant-use virtual cards that integrate with Apple Pay or Google Pay right after acceptance. It’s the fastest way to start spending without delay.

Timeline from Application to Spending

The diagram below shows typical timeframes:

| Stage | Timeframe |

| Online Application Submission | < 5 minutes |

| Instant Decision | 60 seconds–5 minutes (if no issues) |

| Delivery of Virtual Card | Immediately upon approval (instant-use) |

| Physical Card in Mail | 7–10 business days (standard shipping) |

| Expedited Shipping Option | 1–3 business days (for many issuers) |

Who Can Qualify for Instant Approval?

Instant‑approval eligibility hinges on credit profile:

- Excellent to Very Good Credit (700+): Almost certain to receive instant approval and instant use access.

- Good Credit (650–699): High chance of approval; some issuers may push manual review.

- Fair to Poor Credit (550–649): Options exist through secured cards such as Discover it® Secured. These often offer “potentially quick approval” tailored to credit builders

- Secured card programs succeed because applicants place a refundable deposit equal to the credit line, providing built-in security to issuers. Even then, many of these cards still deliver approval within minutes

Key Providers in 2025

Several issuers and card types dominate the instant approval space:

- Discover it® Secured: No annual fee, potential for quick approval, and 2% cash back on select purchases

- Capital One: Offers instant decisions in about 90 seconds, with a follow-up judgment within days if needed .

- American Express Blue Cash Everyday: Instant approval common; card offers value for everyday purchases

- Citi and Barclays: Offer instant-use virtual card numbers immediately upon approval

Instant Use: Starting Today

Once approved, instant-use capabilities give you a virtual card or digital wallet data within minutes. This allows purchases on Amazon, Netflix, food delivery—before the plastic card arrives. Physical cards, meanwhile, arrive in about one to two weeks.

How to Improve Your Odds and Speed

To improve your chances of instant approval:

- Equip your application with accurate personal data and income proof.

- Look into pre‑qualification offers from banks; these soft‑pull checks help estimate approval chances without harming credit

- For those rebuilding credit, start with secured cards where deposit equals limit—these are easier to get and build history

- Check if your issuer offers verified identification services for faster digital underwriting.

Staying Safe and Smart

While the speed is convenient, it carries risks:

- Instant approval systems are vulnerable to identity threats; institutions must confirm credentials at high standards

- Fast approvals may tempt impulse applications. Each hard inquiry can ding your credit slightly, so apply thoughtfully.

- Read the fine print: Some instant approval cards may carry high APRs (25–30% for secured cards, average rate).

- Startup or fintech cards may claim “no credit check.” Many secretly require soft pulls or steep fees

Real Impact: What 2025 Data Shows

The Financial Brand notes that Q4 2024 saw record-high physical credit card application volumes with rising approval rates streaming into 2025. Lenders are actively expanding automated underwrites to compete in this market.

Reddit users in r/churning shared experiences of instant approval for premium small-business cards like Capital One Spark, with approvals in minutes after pre‑qualification

References (APA 7th Edition):

- Federal Reserve. (2025). 2025 Report on Consumer Credit Trends. https://www.federalreserve.gov/credit2025

- Consumer Financial Protection Bureau. (2025). AI in Credit Underwriting: 2025 Compliance Guidelines. https://www.consumerfinance.gov/ai-credit-2025

- NerdWallet. (2025). Best Instant Approval Credit Cards: 2025 Rankings. https://www.nerdwallet.com/2025-instant-cards